Project CHALLENGE

We were tasked to address issues relating to the onboarding journey, from the time a HNW individual think about Bank X until an account is successfully opened, with a head start on these problems:

Waiting time

Long onboarding process with multiple manual touch points impacting both client and RM experience

Accountability

Lack of end-to-end accountability across the client journey

Outdated Information

Absence of real-time capability for ongoing transaction and dynamic client risk-monitoring

Solutions and impacts

With the new online onboarding portal and improved working processes, bank staff can now collaborate with other departments, monitor and speed up the progress of a Client Profile creation journey by significantly cutting down the waiting time from 3 months to a few weeks. Through the portal, customers have the flexibility to self-serve and experience greater visibility of their account progress without having to rely on their RMs.

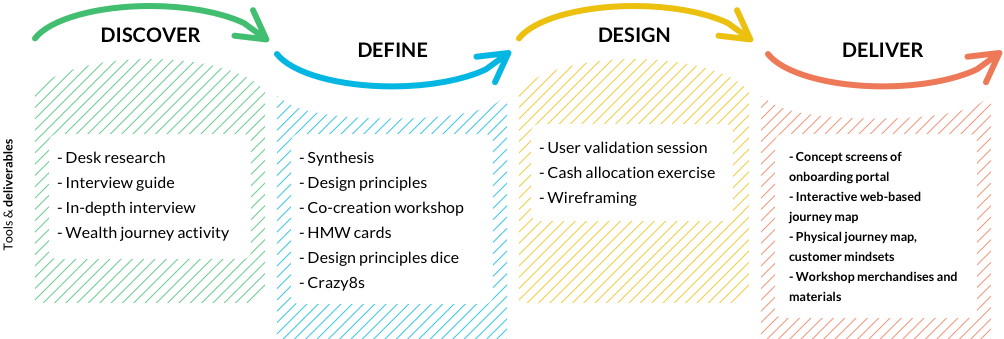

Discovery

With the goal of transforming Bank X’s client lifecycle journey, the team dived straight into the issues on the onboarding journey — from the time they think about Bank X to the time their account is opened. Ethnographic research was conducted in 2 weeks, across 2 countries (Singapore and Hong Kong) with high net worth individuals and Bank X’s staff from relationship managers (RM) to supporting compliance officers. Interviews were conducted in two different languages; English and Mandarin. In order to quickly understand Bank X’s environment and work processes, we leveraged on the staff’s financial knowledge by checking in and shadowed multiple compliance officers on a daily basis.

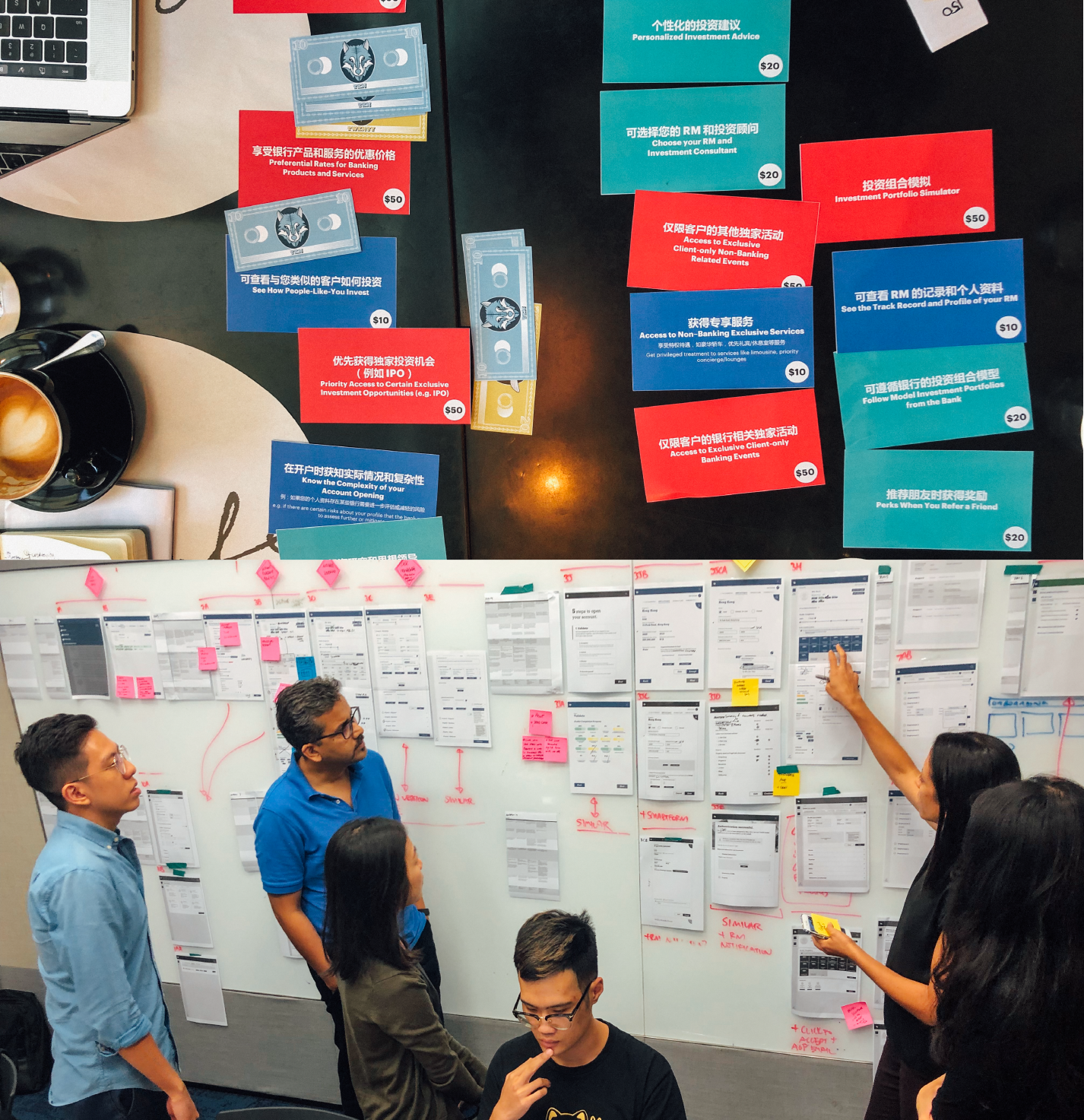

Led by our design director, we created interview guides to learn and understand the dynamics within the different teams in the bank, between the bank and its customers, as well as their perceptions of and experiences with other banks. Our understanding of the onboarding process slowly took shape as we slowly fill up a journey map after each interview session. During these few weeks, our initial assumptions and questions were challenged, debunked, answered and proven. From identifying a prospect to post account opening, we made sure to document every single step in this E2E journey which led us to rounds of synthesis in the later stage.

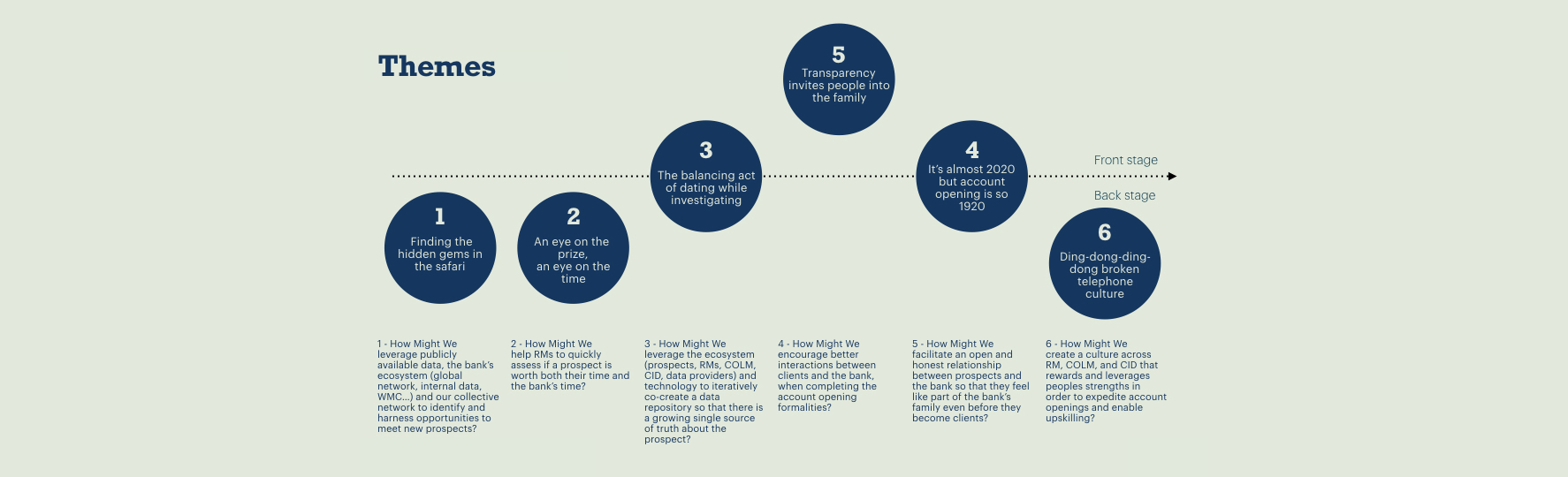

Defining — insights

1. Clients are not all untouchable emperors

2. Overprotecting the RMs only creates more unnecessary steps

3. More red carpet cases, more workload

1. Clients are not all untouchable emperors

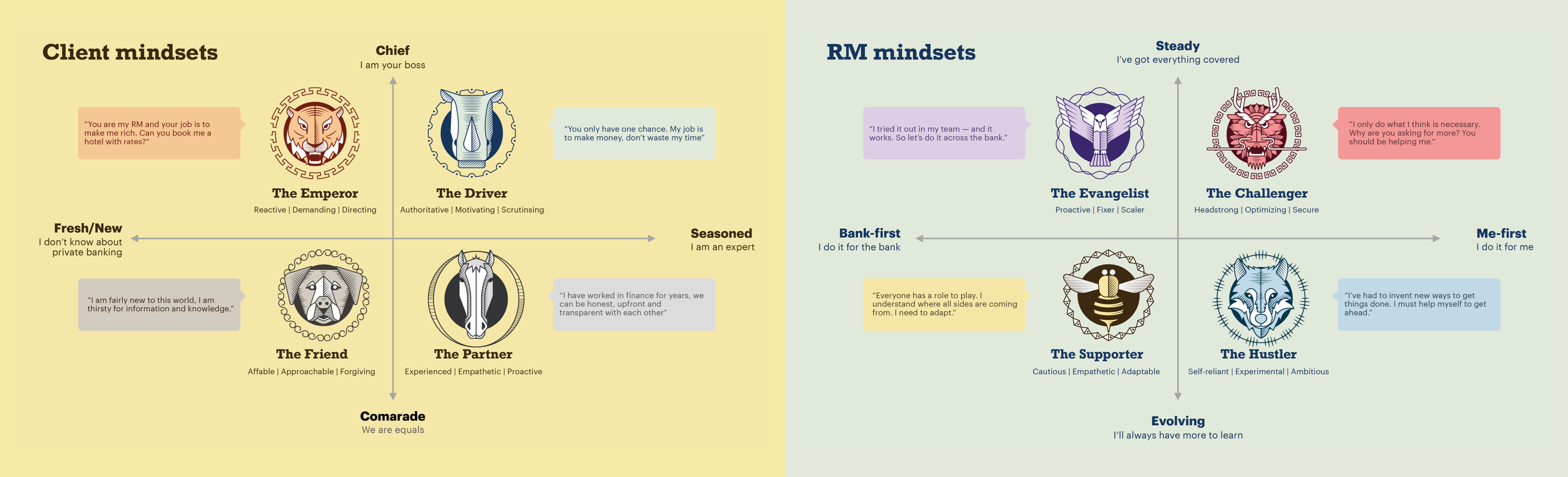

Contrary to what we believe, HNW clients are very experienced with digital services like Netflix and Spotify just like you and I. Many of them cross-references and expect these digital experiences with banks too. They are also comfortable with data sharing within the bank and do not expect to have their data treated with absolute secrecy. While most of us think that the wealthy are all high maintenance and needs to be serviced, to our surprise, many are very willing to collaborate with RMs and self-service whenever needed.

2. Overprotecting the RMs only creates more unnecessary steps

The bank introduced a new onboarding document preparation process for the RM. Instead of preparing a list of documents through the assistant RMs, RMs have to leverage on the compliance team to do so. However, this creates an additional step and queue for the very experienced RMs who are already very familiar with the documents. As for younger RMs, it also means that they will overlook the product section, as opposed to what some RMs are interested in exploring more about this topic at this stage.

3. More red carpet cases from the RMs, more workload for the compliance officers at the end of the chain

Ultra HNW clients or special clients receive “red carpet” treatment as their onboarding journeys are expedited. In Hong Kong and China where there are many such clients, compliance officers need to stop all other cases and dedicate themselves to clear the clients quickly, causing an inevitable delay of the other processes while being overloaded with work.

There are two different groups of officers within the compliance team. One gathers all the necessary client information to complete the Know-your-customer (KYC) process while the other checks and approves the applicants. In order to clear these red carpet cases quickly with no mistakes and little inquiries from Team B, Team A tends to gather too much information more than needed, causing a massive workload to Team B to look through the details. These side effects usually cause a massive delay to the other normal clients, resulting in disgruntled applicants who decide to leave and switch banks as well as a team of stressful and upset officers who struggle to reach their KPIs.